Vincent Mok

Vincent Mok

Connecting Posit Workbench (RStudio) to GitHub with HTTPS

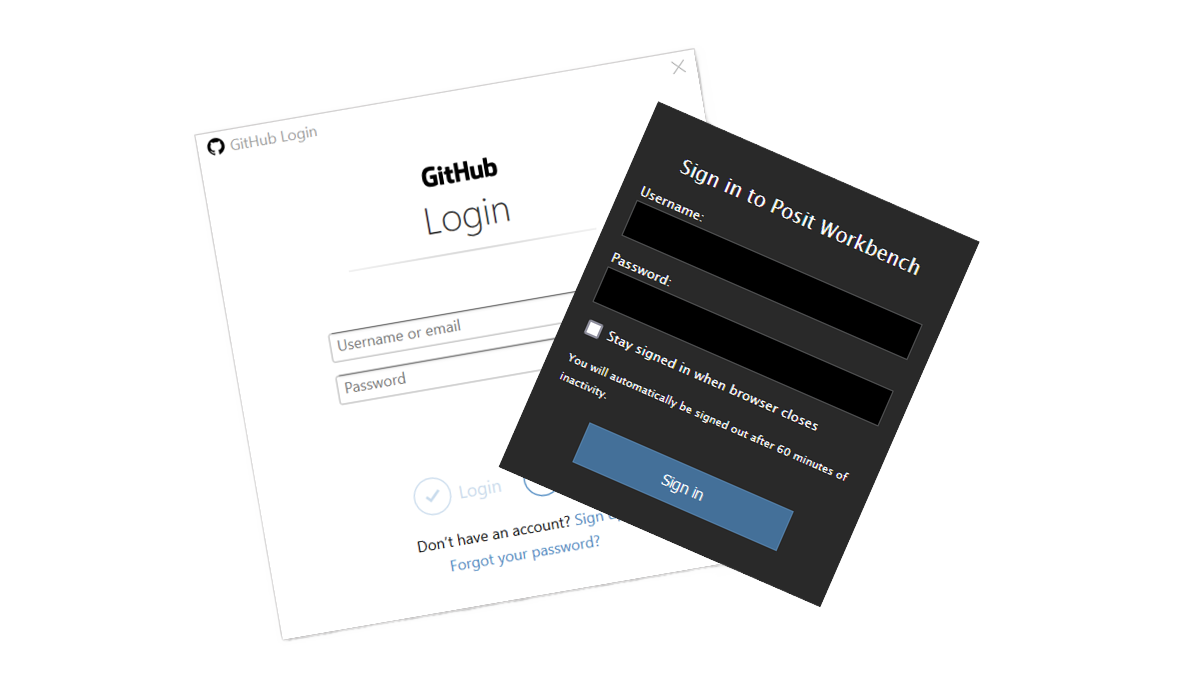

If you're an RStudio user using Posit Workbench and want to use GitHub for source control (you should), this is the guide for you. There are two ways...

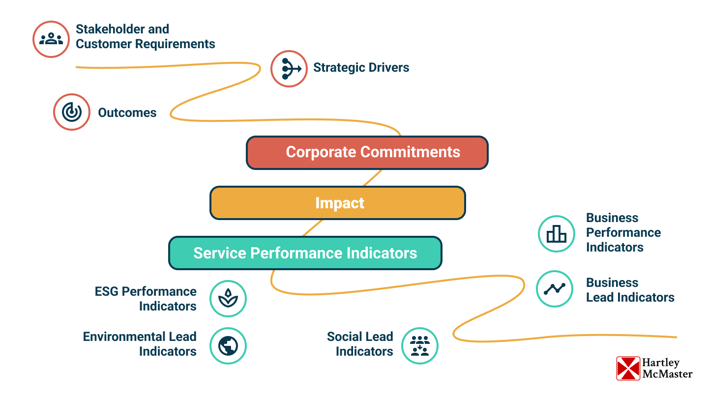

If there seems to be confusion around the practical implications of ESG, much of it stems from the demands it places on finance professionals to acquaint themselves with knowledge extending beyond what is traditionally considered ‘business fundamentals’. For the first time, financial functions are having to contend with the minute details of operational matters. This involves the extensive work necessary to build visibility into all material aspects of operations and requires that they engage with stakeholders in a way they never needed to before. Fortunately, there are many historic examples of ESG being integrated into financial decision-making from regulated utilities.

ESG investment would benefit from existing methodologies developed for regulatory investment planning in the utilities sector;

The finance community has hastily poured billions into ESG-focused investment funds. The optimist might say that this is an instance of financial incentives aligning with “doing the right thing”; that it proves that regulatory intervention isn’t necessary to address critical global issues such as climate change. The skeptic might, on the other hand, argue that ESG investments are a thin veneer of ethics meant to placate guilty consciences or preempt public opprobrium; that it’s a concept adjacent to “greenwashing”.

Our own interest isn’t in making these types of proclamations, but to share a glimpse of what Operational ESG or Impact Investment will look like in the coming decade.

The asset investment planning exercise undertaken at utilities is the mechanism by which they balance investment requirements. Balancing, in the case of utilities, means ensuring they are not underinvesting – thereby risking service disruption – nor overinvesting – thereby undermining financial performance. While this may appear orthogonal to the ESG investment case, understanding how utilities have dealt with, defined, and quantified measurements around “service” and “financial performance” is directly relevant to how an organization might want to assess materiality and impact.

For instance, ask yourself what the impact on your community would be if there was an electrical blackout. What if water service was disrupted? Or perhaps there’s a leak in a gas main. Now ask yourself what the impact cost of these scenarios would be and what you would be willing to pay to avoid them. These questions hint at the tremendous amount of work necessary to define and quantify the contours around the concepts of “service” and “financial performance”

Properly conducted, these investment planning exercises allow utilities to quantify and monetize the risk of asset/service failure, ensuring they have long-term visibility into their investment requirements (e.g. long-term debt load) and to build stakeholder consensus around, for instance, the right level of tariffs necessary to support these investments. Furthermore, by developing these definitions into a composite value measurement across the organization, investments can be assessed on a common cost-benefit basis across asset classes in a manner that is sound, transparent, defensible, and also incorporates diverse viewpoints from stakeholder networks, including the communities served.

If you’ve spent any time thinking about ESG issues, it should be readily apparent how these approaches apply to impact investment. Yes, the stakeholder landscape might look different, but the underlying techniques for decision-making will mimic those already being used in regulatory investment planning. The question is thus less around what this will look like, and more around whether organizations will ultimately commit to this type of approach. For instance, despite these methods being well-developed within the utilities space, their adoption has still been largely limited to levels commensurate with the level of regulatory scrutiny. It’s a virtual certainty that much of this dynamic will be reflected within the ESG space in the coming years.

A key difference, however, is that without an independent intermediary (such as a regulator) to – in effect – “normalize” ESG output across different sectors, industries, and organizations, it will be impossible for ESG investors to have a common-basis understanding of the real risk factors behind their financial assets (or more specifically, the underlying real assets). The rote answer to these concerns has largely been that standardization of metrics is the gold standard and that credit rating agencies will function as pseudo-regulatory bodies. However, few people within operational circles believe that standardization (or credit rating agencies for that matter) will get us anywhere the level of resolution needed to accurately track impact, much less make impact investments.

Instead, we are likely to see a small cadre of (financial) asset management firms develop capabilities – internally or through partnerships – to assess the (real) asset management capabilities of their portfolio companies and – where feasible – expand their risk management frameworks to incorporate real asset data. In other words, there will be no shortcut to understanding actual ESG risks without developing true operational knowledge. The application of real asset management practices to the ESG investment landscape will thus be concentrated with top-tier financial firms or specialist investment firms (e.g. climate change funds). For most other companies, there will be little incentive to adopt or invest in these capabilities unless (a) they are high profile and under extreme scrutiny, (b) they anticipate regulatory action within their industry or market or (c) they genuinely believe in the concepts of ESG and transparency.

All other firms will rely on standardized metrics for ESG reporting. The extent to which these reporting standards will make an impact on E, S, or G remains to be seen. However, given the top-down nature of these frameworks, it is easy to imagine the use of financial engineering techniques to clear ‘ESG hurdles’. For investment firms that genuinely want to be responsible custodians, now is the time to build your knowledge around operational capabilities – developing expert knowledge is never a bad investment.

If you're an RStudio user using Posit Workbench and want to use GitHub for source control (you should), this is the guide for you. There are two ways...

Many companies investing in data analytics struggle to achieve the full value of their investment, perhaps even becoming disillusioned. To understand...

We are cursed to live in interesting times. As I write this, a war in Ukraine rumbles on, we sit on the tail of a pandemic and at the jaws of a...